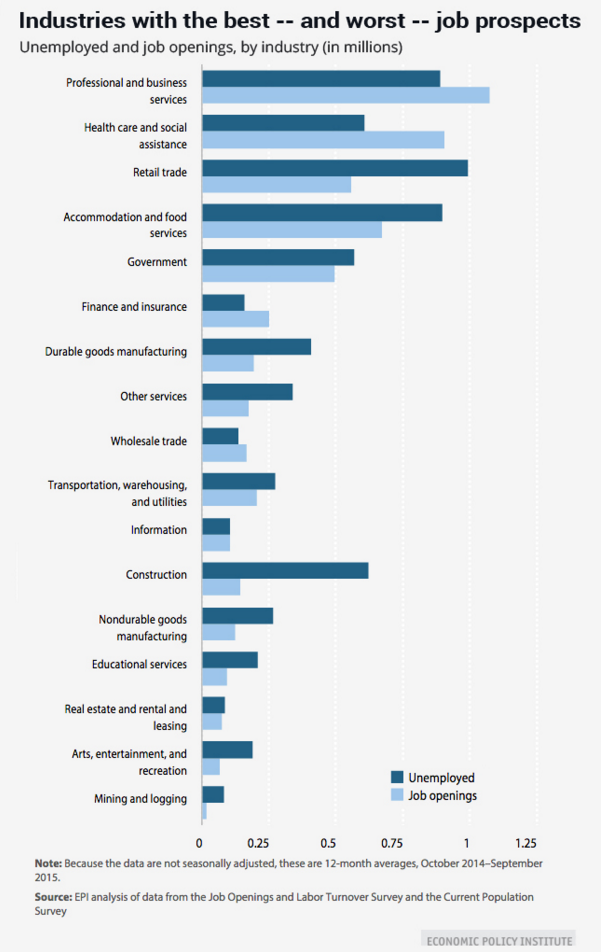

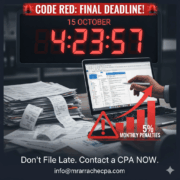

CODE RED: The Final Tax Deadline is HERE. File or Face Penalties.

You filed your extension—good. Now, it’s October 11th, and the true deadline is staring you down. Tax season is over for everyone else, but for you, the clock is running out on the Failure to File Penalty, which is 10 times higher than the penalty for late payment.

This is a Code Red. You need an urgent strategy to file your return immediately and prevent penalties from accruing.

The Urgent Pain Point: What Happens on October 15th?

When you filed Form 4868, you successfully avoided the Failure to File penalty back in April. However, failing to file by the extended October 15th deadline activates the most costly penalties retroactive to the original April deadline.

| Penalty | Rate | Costly Trigger |

| Failure to File (Worst Penalty) | 5% of the unpaid tax for each month or part of a month the return is late. | Missing the October 15th deadline. |

| Failure to Pay (Lesser Penalty) | 0.5% of the unpaid tax for each month or part of a month it remains unpaid. | This continues to accrue even with an extension, but is far smaller than the Failure to File penalty. |

The Stakes: If you owe the IRS, missing the October deadline triggers the massive 5% per month Failure to File penalty, compounded with the Failure to Pay penalty and daily interest charges. Your total penalty could climb to 25% of your unpaid tax very quickly.

Your Immediate Action Plan to Stop Penalties

Your goal is simple: File. Now. File the return, even if you can’t pay the balance in full. Filing stops the 5% penalty immediately.

1. Prioritize Documentation & Organization

Do not waste time trying to perfectly calculate every deduction. Focus on accurately reporting all income (W-2s, 1099s, K-1s) and high-priority deductions (like mortgage interest and estimated payments).

- Action: Find and scan (or take clear photos of) your income documents. File your tax return using this information as soon as possible.

2. File Electronically (The Only Option)

Paper returns take weeks or months to process. E-filing is the fastest way to get your return to the IRS and secure that October 15th timestamp, which is what matters most.

- Action: E-file your return now. The IRS Direct File service is available through October 15th for qualified taxpayers, as are major software platforms.

3. Pay What You Can to Minimize Interest

The Failure to Pay penalty is based on your unpaid balance. Reduce the base amount of the penalty and interest by paying any amount you can with the return.

- Action: If you owe $5,000 but can pay $1,000 today, pay it. That interest and penalty stops accruing on that $1,000 immediately.

What to Do If You Owe and Can’t Pay

Successfully filing by October 15th gives you leverage when dealing with the IRS. Don’t let a payment issue stop you from filing.

Option A: Online Payment Agreement

The IRS offers several payment options, including short-term and long-term Installment Agreements. You can often apply online if you owe less than $50,000.

- Benefit: Setting up a payment plan reduces the Failure to Pay penalty rate from 0.5% to 0.25% per month.

Option B: Penalty Relief

Once you have filed your return and established a payment plan, you can request penalty relief.

- First-Time Abatement (FTA): If you have a clean compliance record (no prior penalties in the past three years), you may qualify to have the initial penalties waived.

- Reasonable Cause: If the delay was due to circumstances beyond your control (e.g., serious illness, death in the family, or a natural disaster), you can formally request a penalty waiver by providing documentation to the IRS.

Do not wait until October 16th. Your priority is to file the tax return before midnight on October 15th to lock in your compliance and avoid the harshest penalties the IRS charges.

Take Action: Don’t Face the IRS Alone

If the complexity of your return is what is slowing you down—especially with rental properties, K-1s, or business income—the risk of not filing far outweighs the cost of professional help. Get your documents to an expert now to ensure the October 15th deadline is met. Reach out to us today to see how we can help you along the way.

About the Author

Michael R. Arrache, CPA, EA, DRE

As a Certified Public Accountant (CPA), Enrolled Agent (EA), and licensed Realtor, I am a tax expert who works closely with small business owners and real estate investors. My firm, Arrache CPA, Inc. dba Mr. Smart Tax, provides a range of specialized financial and real estate services, including tax planning, business transactions, and real estate advisory. With over 15 years of experience, my mission is to help clients achieve their financial and business goals by providing strategic advice and tailored solutions. I write these articles to serve as a starting point to guide you through the business or real estate process, and I am committed to providing the strategic guidance you need to help preserve and grow your wealth.

Contact us at info@mrarrachecpa.com.